MSMEs Struggle with Export–Import Finance & FTAs

MSMEs Struggle with Export–Import Finance & FTAs

Why Indian MSMEs Struggle with Export–Import Finance & FTAs

The Silent Bottleneck Holding Back India's Global Trade

India does not lack export–import finance schemes.

India does not lack trade agreements.

India does not lack policy intent.

What India lacks is last-mile execution.

Despite dozens of schemes from the Government of India, RBI, EXIM Bank, ECGC, and public sector banks — and despite multiple Free Trade Agreements (FTAs) — the majority of Indian MSMEs are structurally unable to access, apply, and benefit from these advantages.

This is not a funding problem.

It is a system design problem.

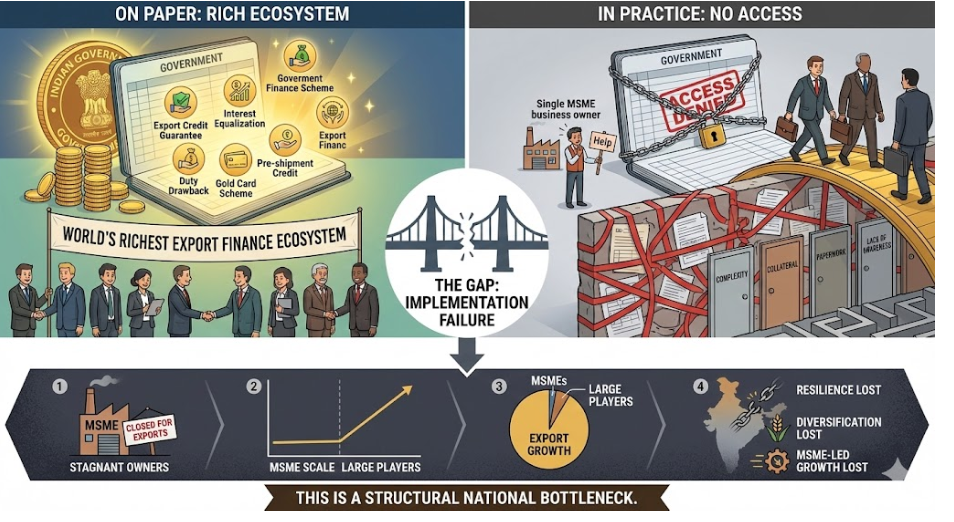

I. The Core Reality: Schemes Exist, Access Does Not

On paper, India has one of the richest export finance ecosystems in the world.

In practice, most MSMEs never fully benefit.

As a result:

- MSMEs don't enter exports

- Existing exporters don't scale

- Export growth remains concentrated among large players

- India loses diversification, resilience, and MSME-led growth

This is a structural national bottleneck.

Core Problems MSMEs Face in Getting Export–Import Finance

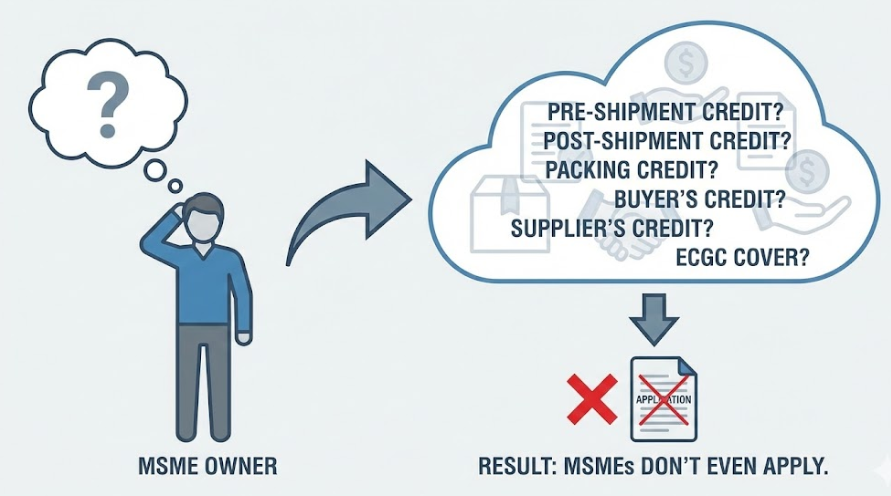

1️⃣ Lack of Awareness & Clarity

Most MSMEs:

- Don't know which scheme applies to them

- Don't understand the difference between:

- Pre-shipment credit

- Post-shipment credit

- Packing credit

- Buyer's credit

- Supplier's credit

- Are unaware of ECGC cover requirements

Result:

MSMEs don't even apply.

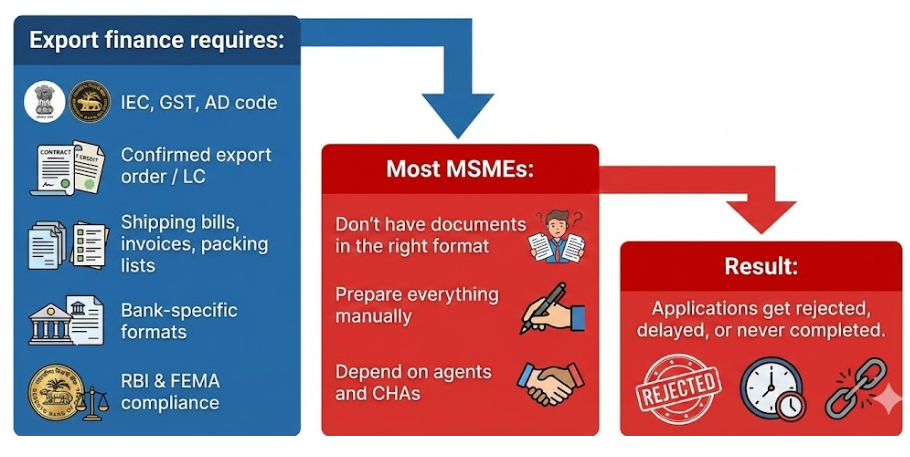

2️⃣ Heavy Documentation & Compliance Burden

Export finance requires:

- IEC, GST, AD code

- Confirmed export order / LC

- Shipping bills, invoices, packing lists

- Bank-specific formats

- RBI & FEMA compliance

Most MSMEs:

- Don't have documents in the right format

- Prepare everything manually

- Depend on agents and CHAs

Result:

Applications get rejected, delayed, or never completed.

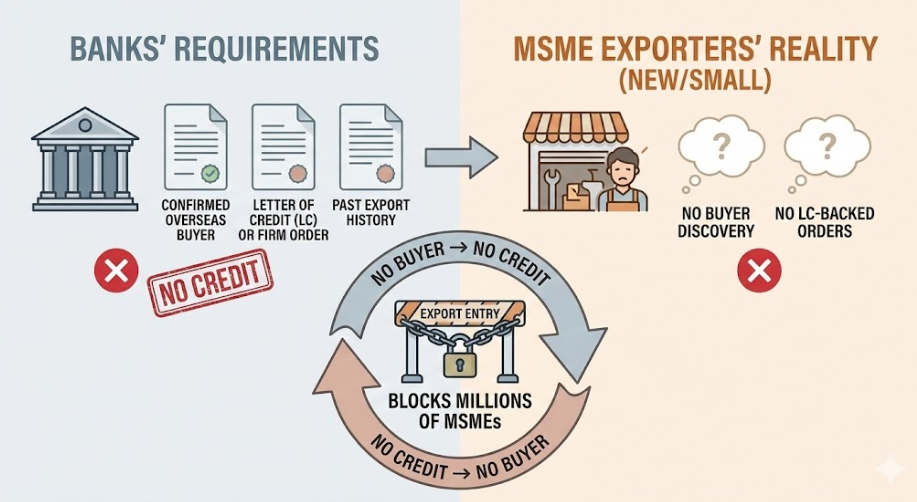

3️⃣ No Confirmed Buyers = No Credit (The Chicken-and-Egg Trap)

Banks usually ask for:

- Confirmed overseas buyer

- Letter of Credit (LC) or firm order

- Past export history

New or small exporters:

- Don't have buyer discovery

- Don't have LC-backed orders

Result:

No buyer → no credit

No credit → no buyer

This single loop blocks millions of MSMEs from entering exports.

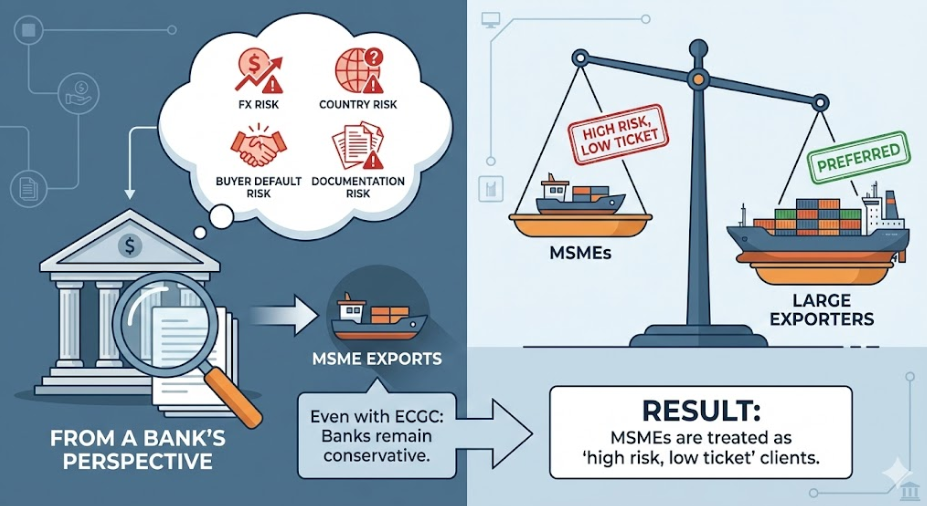

4️⃣ High Risk Perception by Banks

From a bank's perspective:

- MSME exports = higher FX risk

- Country risk

- Buyer default risk

- Documentation risk

Even with ECGC:

- Banks remain conservative

- Prefer large, repeat exporters

Result:

MSMEs are treated as "high risk, low ticket" clients.

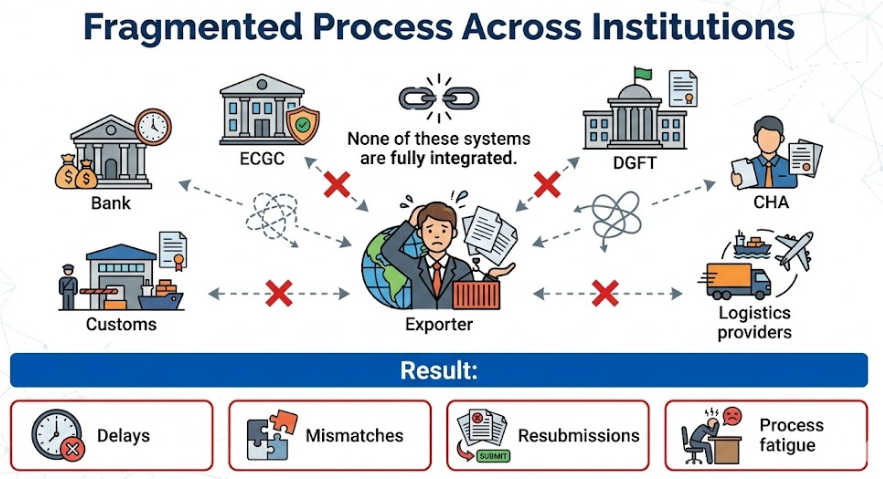

5️⃣ Fragmented Process Across Institutions

An exporter must coordinate with:

- Bank

- ECGC

- DGFT

- Customs

- CHA

- Logistics providers

None of these systems are fully integrated.

Result:

Delays, mismatches, resubmissions, and process fatigue.

6️⃣ Delays in Credit Disbursement

Even when approved:

- Pre-shipment credit is delayed

- Post-shipment realization is slow

- GST & drawback refunds take time

Result:

Working capital stress.

7️⃣ Collateral & Margin Requirements

Despite "collateral-free" messaging:

Banks often still ask for:

- Property

- FD margin

- Personal guarantees

Small exporters:

- Lack collateral

- Operate on thin margins

Result:

They opt out of formal export finance.

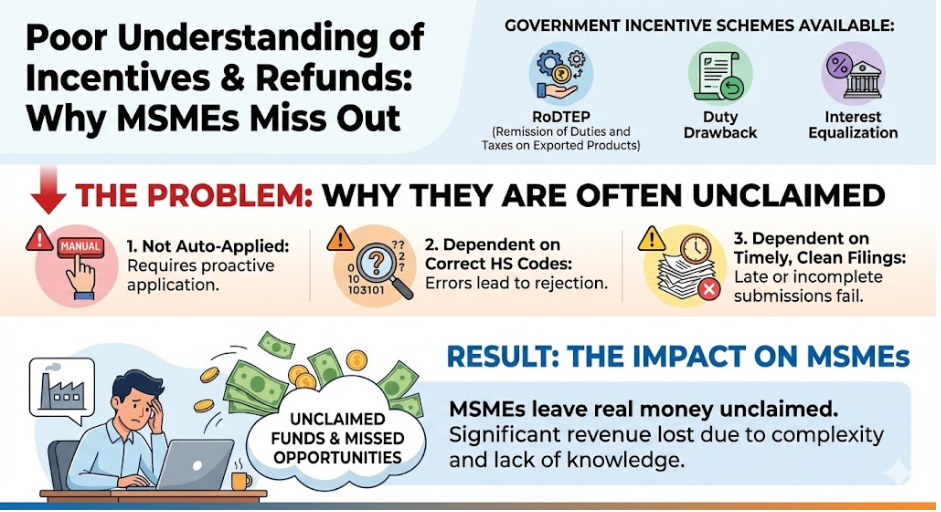

8️⃣ Poor Understanding of Incentives & Refunds

Schemes like:

- RoDTEP

- Duty Drawback

- Interest Equalization

Are:

- Not auto-applied

- Dependent on correct HS codes

- Dependent on timely, clean filings

Result:

MSMEs leave real money unclaimed.

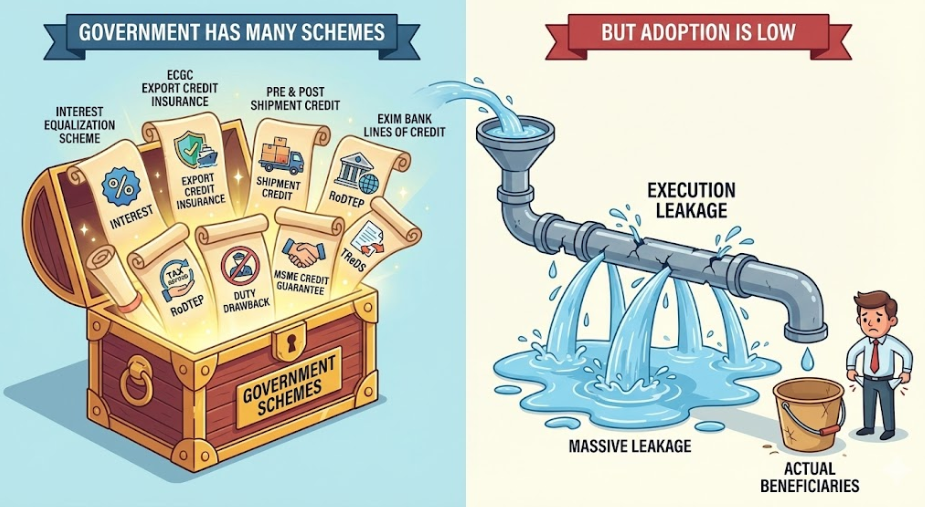

II. Government Has Many Schemes — But Adoption Is Low

Major schemes include:

- Interest Equalization Scheme

- ECGC export credit insurance

- Pre & Post Shipment Credit (RBI-regulated)

- EXIM Bank Lines of Credit

- RoDTEP

- Duty Drawback

- MSME Credit Guarantee schemes

- TReDS (invoice discounting)

Yet execution leakage remains massive.

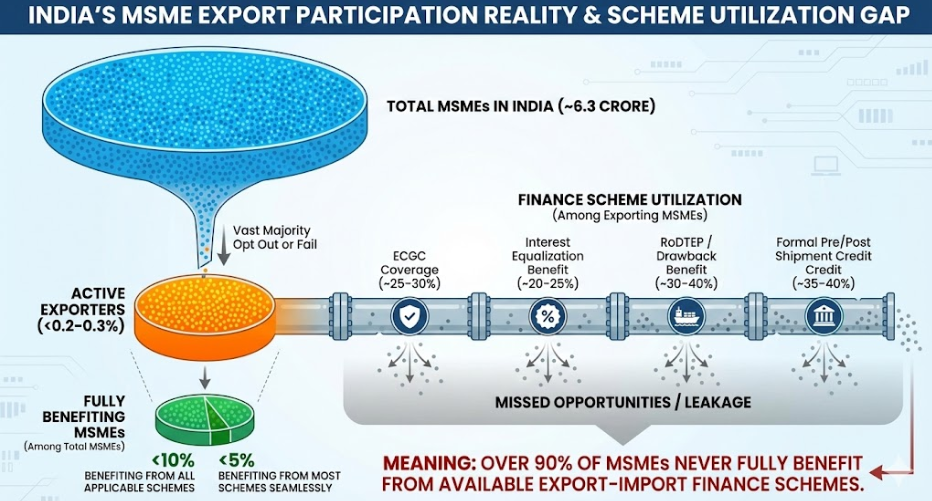

III. What Percentage of MSMEs Actually Benefit? (Hard Truth)

Export Participation Reality

- ~6.3 crore MSMEs in India

- Less than 0.2–0.3% are active exporters

Finance Scheme Utilization (Broad, Conservative Estimates)

Among exporting MSMEs:

- ECGC coverage: ~25–30%

- Interest Equalization benefit: ~20–25%

- RoDTEP / Drawback fully claimed correctly: ~30–40%

- Formal pre/post shipment credit access: ~35–40%

Among total MSMEs:

- Benefiting from all applicable schemes: less than 10%

- Benefiting from most schemes seamlessly: less than 5%

Meaning:

Over 90% of MSMEs never fully benefit from available export–import finance schemes.

IV. Why Schemes Don't Reach MSMEs (Root Causes)

- Schemes are information-rich, execution-poor

- No auto-eligibility mapping

- Poor data quality blocks automation

- Too many intermediaries

- Manual, PDF-driven workflows

- No integrated trade + finance + compliance systems

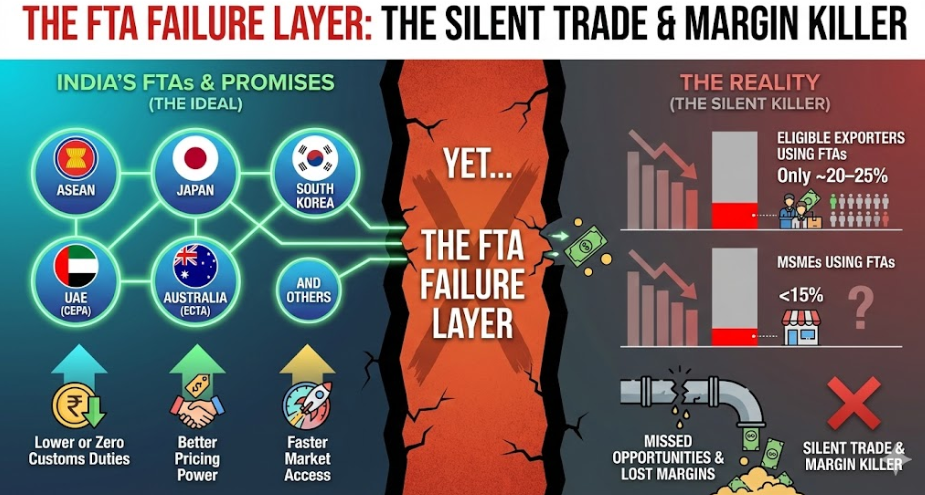

V. The FTA Failure Layer: The Silent Trade & Margin Killer

India has signed multiple FTAs to boost competitiveness:

- ASEAN

- Japan

- South Korea

- UAE (CEPA)

- Australia (ECTA)

- And others

These offer:

- Lower or zero customs duties

- Better pricing power

- Faster market access

Yet…

- Only ~20–25% of eligible exporters use FTAs effectively

- For MSMEs, less than 15%

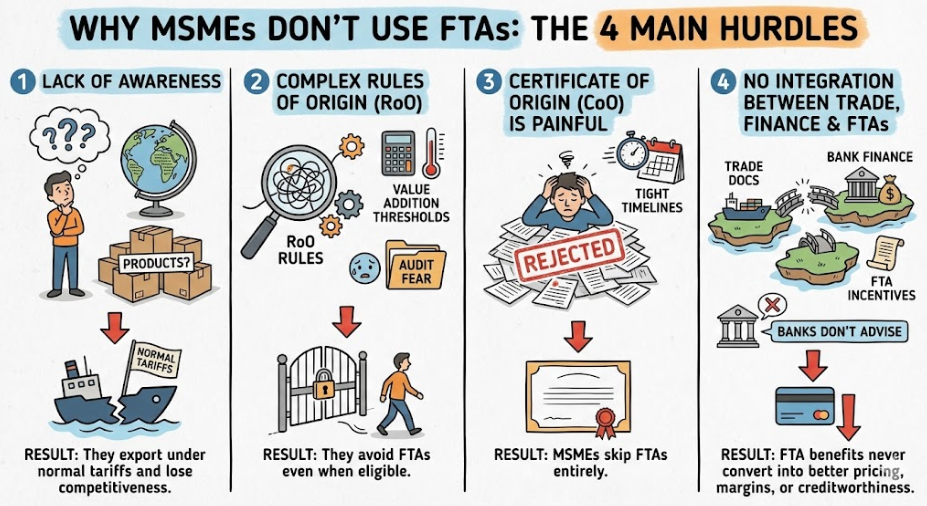

Why MSMEs Don't Use FTAs

1️⃣ Lack of Awareness

- Don't know which FTA applies

- Don't know which products qualify

- Don't know duty benefit value

Result:

They export under normal tariffs and lose competitiveness.

2️⃣ Complex Rules of Origin (RoO)

- Product-specific RoO

- Value-addition thresholds

- HS-code-level compliance

MSMEs:

- Don't understand RoO

- Don't track value addition

- Fear audits and rejection

Result:

They avoid FTAs even when eligible.

3️⃣ Certificate of Origin (CoO) Is Painful

- Manual application

- Error-prone documentation

- Rejections common

- Tight timelines

Result:

MSMEs skip FTAs entirely.

4️⃣ No Integration Between Trade, Finance & FTAs

FTA usage is disconnected from:

- Export documentation

- Bank finance

- Incentive workflows

Banks:

- Don't proactively advise on FTAs

- Don't link FTA benefits to credit

Result:

FTA benefits never convert into better pricing, margins, or creditworthiness.

5️⃣ Poor Data Quality Blocks FTA Automation

FTA requires:

- Accurate HS codes

- Correct origin declarations

- Clean BOM and invoice data

MSMEs submit:

- PDFs

- Inconsistent formats

- Manual documents

Result:

Even eligible exporters fail audits or face rejection.

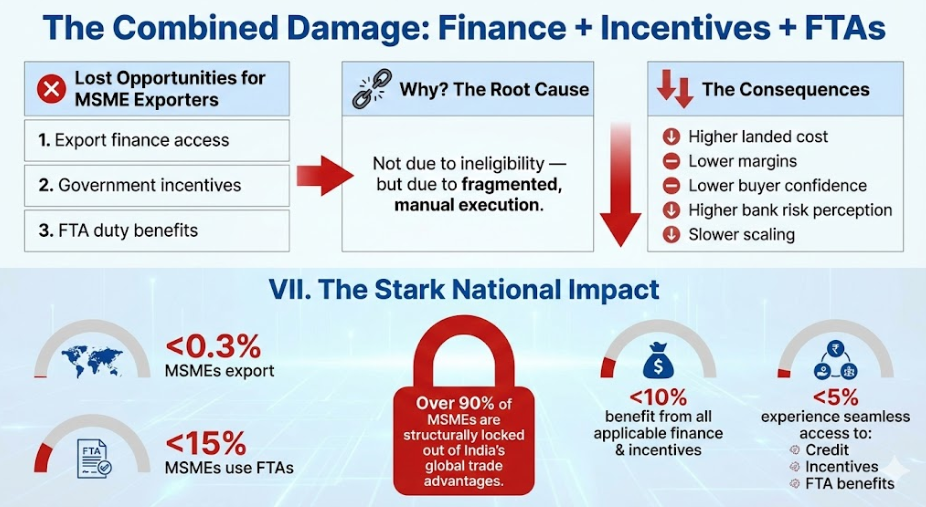

VI. The Combined Damage: Finance + Incentives + FTAs

Today, an MSME exporter often loses simultaneously:

- Export finance access

- Government incentives

- FTA duty benefits

Not due to ineligibility — but due to fragmented, manual execution.

This means:

- Higher landed cost

- Lower margins

- Lower buyer confidence

- Higher bank risk perception

- Slower scaling

VII. The Stark National Impact

Conservatively:

- less than 0.3% MSMEs export

- less than 15% MSMEs use FTAs

- less than 10% benefit from all applicable finance & incentives

- less than 5% experience seamless access to:

- Credit

- Incentives

- FTA benefits

Over 90% of MSMEs are structurally locked out of India's global trade advantages.

VIII. Why This Is a National Growth Problem

When MSMEs can't access:

- Credit

- Incentives

- FTAs

India loses:

- Export diversification

- MSME-led job creation

- Supply-chain resilience

- Competitiveness vs Vietnam, Bangladesh, Thailand

Export growth becomes over-concentrated in large players, increasing systemic risk.

Closing Section

"India has built world-class trade policy, finance schemes, and FTAs.

What MSMEs lack is a system that connects all of them into one executable flow."

This sets up your next blog perfectly:

How ManuDocs unlocks export finance, incentives, and FTA benefits automatically — by fixing data, documentation, buyer discovery, and execution at the source.